How to Start a Budget: A Step-by-Step Guide to Financial Planning and Expense Management

These days, planning is an important part of keeping track of your money in a world where money worries are common. A recent poll found that 62% of Americans live from paycheck to paycheck. This shows how important it is to have a well-thought-out budget. You can reduce stress, improve your financial security, and reach your long-term financial goals if you know how to start a budget a step-by-step guide to financial planning and expense management and choose wisely how to spend and save it. Making a budget is the first thing you should do if you want to get more control over your money, pay off debt, or save for a big buy.

Step 1. What is a Budget and Why Do You Need One?

A budget is basically a plan that helps you keep track of your money coming in and going out, so you don’t spend more than you make. It lets you divide your money into different groups, like saves, bills, and extra spending. Making a budget isn’t just about putting limits on yourself; it’s also about setting up a system that helps you focus your financial goals while still living a comfortable life.

Benefits of Budgeting

- Debt Reduction: By making a budget, you can decide how much of your cash to put toward paying off debt. By taking this consistent method, you can lower your balances over time, which will help you reach financial freedom in the end.

- Emergency Savings: A good budget helps you save money for situations, which gives you peace of mind in case you have to pay for something unexpected.

- Achieving Financial Freedom: After making a budget, you can work toward big financial goals like buying a house, saving, or retiring in style.

Basically, making a budget helps you be more responsible with your money and helps you choose wisely how to spend and save it, which helps you stay on track with your financial goals.

Step 2. Step-by-Step Guide to Creating Your First Budget

Assess Your Financial Situation

It’s important to know where you stand financially before you start making a budget. Start by adding up your monthly income. This covers your main job, any side jobs you have, passive income, and any other money you make. Knowing how much money you make in total helps you make a budget that you can stick to.

- Net Income: This is how much money you have left over after taxes and other automatic withdrawals, like health insurance or retirement contributions.

- Revenue Streams: If you get extra money from stocks, freelancing, or other sources, you should include that in your evaluation.

- Track Your Expenses: Next, keep an eye on where your cash goes. Keep track of all your spending for a month to see trends. It’s possible to keep track of your daily spending with apps like Mint or You Need a Budget (YNAB), or you can just use files like Excel or Google Sheets.

Here are some important groups to keep an eye on::

- Fixed Expenses: These include mortgage or rent payments, utility bills, insurance fees, and loan payments.

- Variable Expenses: These are costs that change from month to month, like food, transportation, or fun things to do

- Categorize Your Expenses: After keeping track of your spending, split it into two main groups: necessary spending and optional spending.

- Essential Expenses: These are prices that can’t be changed, like rent, utilities, groceries, and insurance. To keep up a basic level of living, they need to be paid on a regular basis.

- Discretionary Spending: This includes things like fun, eating out, shopping, and subscriptions that aren’t necessary.

- Set Financial Goals: Setting financial goals is an important part of making a budget. First, make a list of your short- and long-term goals:

- Short-term Goals: Some examples are putting money away for a trip, an emergency fund, or to pay off a credit card.

- Long-term Goals: Some examples are putting money away for retirement, buying a house, or trading to get rich.

- Choose a Budgeting Method :There are various ways to make a budget, and picking the right one for you can help the process go more smoothly and work better. These are three common ways:

Step 1:

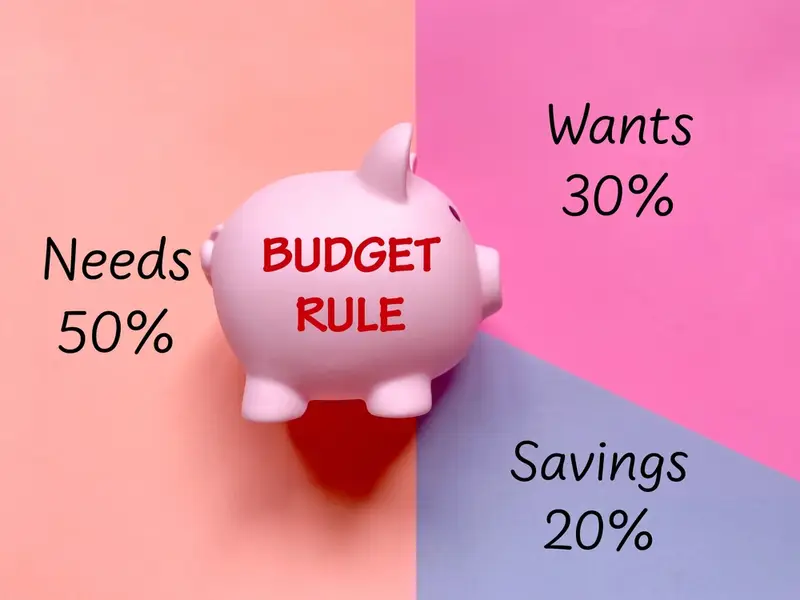

- 50/30/20 Rule: 50/30/20 budgeting is a straightforward approach where you allocate:

- Spend 50% of your income on things you need, like rent, utilities, and food.

- 30% to wants (fun things to do, eating out, and payments).

- 20% to save money and pay off debt.

Step 2:

- Zero-Based Budgeting: For this method to work, you need to give each dollar of your pay a category, such as expenses, savings, or debt. Your goal is to have no income left over after paying all of your bills by the end of the month.

Step 3:

- Envelope System: With this cash-based method, you divide your income into envelopes, with each envelope representing a different type of buying (like groceries or entertainment). That kind of money can’t be spent again until the next month, once the bag is empty. Choose the method that works best for your financial situation and goals.

- Monitor and Adjust: Making a budget is a constant process, not a one-time thing. At the end of each month, look over your budget to see how you’re doing and make any changes that are needed. If things in your life change, like getting a raise in pay, having to pay for something unexpected, or the way your family works, you may need to make changes to your budget. You can stay on track to reach your goals if you check in on your progress often.

Reviewing and making changes to the budget are important for keeping it reasonable and useful. Don’t be afraid to change the ways you spend your money if you need to.

Step 3. Tools and Resources for Effective Budgeting

While you can make and stick to a budget by hand, there are a few tools that can make the process easier and more effective:

- Budgeting Apps: By connecting to your bank accounts, apps like Mint, YNAB (You Need A Budget), and Pocket guard make it easy to keep track of your income and spending. These tools help you stay on track with your finances and give you useful information about how you spend your money.

- Spreadsheets: If you’d rather do it yourself, you can find free models for budget spreadsheets online. These can be changed to fit your specific money needs.

- Expense Tracker Apps: People who want to keep a closer eye on their spending in real time should use apps like Wally or Expensify.

These tools help you stay organized and save time when making a budget.

Step 4. Tips to Stick to Your Budget

Keeping to a budget can be hard, especially when you want to give in to desire. Here are some things you can do to stay committed:

- Automate Savings and Bill Payments: To make sure you stay on track, set up regular bill payments or transfers to your savings account.

- Avoid Impulse Purchases: Don’t buy something on a whim by following the 24-hour rule. If you want to buy something that isn’t necessary, wait 24 hours before making a choice.

- Celebrate Small Wins: When you reach a goal or pay off a credit card, that’s a big deal to celebrate. This keeps you focused and encourages good behavior.

Step 5. Common Budgeting Mistakes to Avoid

It’s possible for even skilled budgeters to get caught. Don’t make these mistakes, and learn how to avoid them:

- Underestimating Expenses: Don’t forget to include costs that don’t happen very often, like car repairs, vacations, or holidays. If you haven’t planned for these, they can throw off your spending.

- Ignoring Flexible Spending: It is important to leave some room in your budget for fun and relaxation. Being too set in your ways can make you angry and tired.

- Neglecting to Track Expenses Regularly: Keeping track of your spending is important for figuring out how you spend your money and making changes to your budget as needed.

Conclusion

Making a budget is a great way to keep track of your money and become financially free. You can get more control over your money and get closer to your financial goals if you keep track of your income and spending, set goals, and use the right budgeting method. Beginning right now will benefit you in the long run.

FAQs About Budgeting

How much should I save each month?

You should try to save 20% of your monthly income as a general rule. Change this to fit your interests and financial goals.

What if my income is irregular?

If your monthly income changes, use Zero-Based Budgeting to decide how to spend your money based on the amount you make the least each month. This will help you stay on track even when money is tight.

How do I handle unexpected expenses?

Set aside money in your budget for an emergency fund. Try to save enough money to cover your living costs for three to six months in case something comes up.